25 May 2021 | Update

New VAT regulations for shipments from non-EU countries as of 1 July 2021

Why does the exemption amount cease to apply?

The removal of the exemption limit is intended to ensure that goods imported from non-EU countries are not subject to preferential VAT treatment compared to goods purchased within the EU.

What does this mean for me as a consignee?

From 1 July 2021 you as a consignee will have to pay taxes on goods from a non-EU country if they exceed a value of 1 euro. You can pay the taxes conveniently via our secure payment platform, unless they have already been paid by the shipper of the goods. This is the case, for example, if you are buying goods worth €150 or less outside the EU and the seller is registered in the new VAT system and uses the one-stop shop for import (IOSS.Import-One-stop-shop). If the sender is not IOSS-registered, you as the consignee will have to pay the import VAT and possible customs duties, which we will have to bill you for.

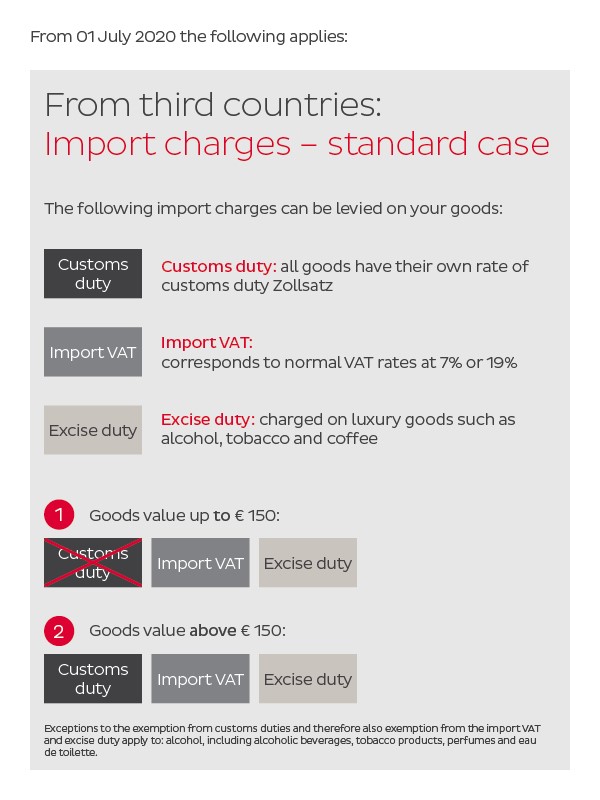

How are import taxes calculated?

The goods value of the consignment is decisive for the calculation of the import VAT. The decisive factor is therefore the amount actually paid to receive the goods. If the value of the goods is up to 150 euros, the import continues to be duty-free. This value limit will remain in place after 1 July 2021. Only the import VAT of 19 per cent or 7 per cent (e.g. for books) and possibly excise duties, for example on alcohol and alcoholic products, perfume and tobacco products must be paid.